#047 Constructing Moats using the Value Proposition Stack: A Cornerstone Perspective

Fri, 26 Sep 2025 11:17:02 GMT

Cornerstone Ventures

We had published our thinking on the Value Proposition Model a few weeks back. This framework has generated a lot of conversation, some positive and some critical but constructive. Happy to continue the conversation forward. So here’s some deeper dives into the competitive moats that we see founders experimenting with.

But first here are some comments that we heard:

- The Value Proposition Stack offers a logical hierarchy that makes intuitive sense - moving from operational efficiency at the base to full ecosystem ownership at the top. The quantitative examples effectively illustrate how value capture increases dramatically as you move up the stack, from $0.10 at the process layer to $100 at the product/platform layer.

- The portfolio company examples are well-chosen and clearly demonstrate each layer. Companies like Mystifly (marketplace) and OfBusiness (product/platform) provide concrete illustrations of the concepts.

Some other critical observations that we heard:

- The framework heavily favors higher layers, which makes sense from a venture capital perspective seeking outsized returns. However, this view may undervalue the strategic importance and defensibility that can exist in lower layers, particularly when they involve deep domain expertise or proprietary technology.

- The assertion that the process enablement layer is “highly susceptible to AI-driven disruption” while higher layers are more resilient may have some exceptions. For instance, AI could not only catalyse but sometimes disrupt marketplace dynamics (through better matching algorithms available to everyone) or create new direct-to-consumer models that bypass existing platforms entirely.

- Additionally, the linear progression implied by the stack may not be a hundred percent achievable. Some successful companies operate across multiple layers simultaneously from the start, and moving “up” the stack altogether isn’t always the optimal strategy due to market needs or could require different capabilities, capital structures, and risk profiles.

- One always needs to consider execution risk - a poorly executed marketplace can be less valuable than a brilliantly executed process optimization tool. Market timing, team quality, and competitive dynamics matter as much as which layer you operate in.

- An additional ask from various folks who have reached out is that we haven’t discussed capital requirements and time horizons for each layer. Marketplace and platform businesses typically require significantly more capital and longer development cycles than process enablement solutions. We plan to address this in a future post, including how we double down when we see the right pieces coming together.

- Another observation that we have heard is - A large, underserved market in the process layer might offer better returns than a smaller market at the platform layer. True, but it also attracts more competition and is prone to erode in value over time.

The application of this model is not an exact science, but a lot of art that also comes in from our investment teams, who put in a fair bit of consideration around capital requirements/availability, founding team, execution quality and shifting market dynamics. We use the framework as one of the tools in our investment decisioning process that is applied thoughtfully rather than prescriptively, recognizing that exceptional execution and market dynamics can create outlier success at any layer.

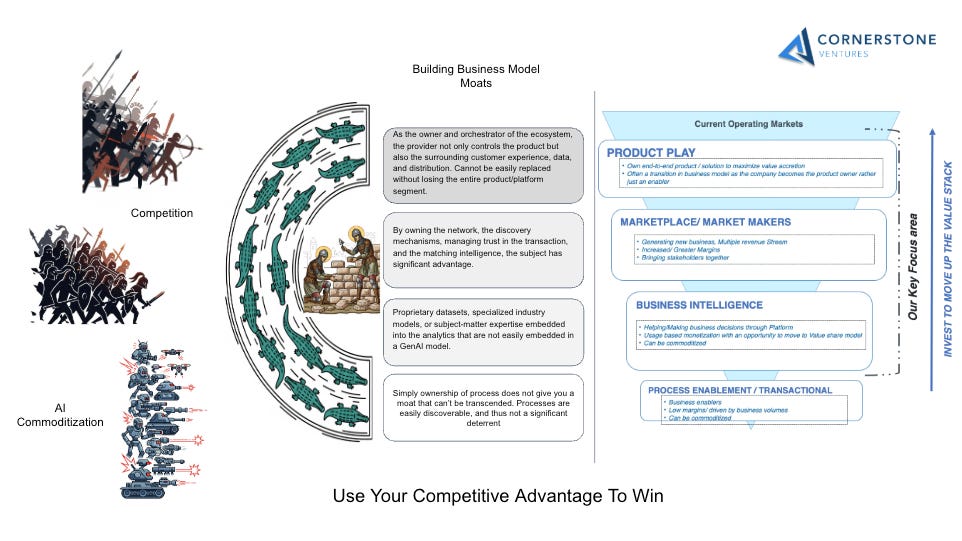

Diving a little deeper into the defensive moats available at each layer of the Value Proposition Stack to protect against Competition and AI commoditization:

1. Process Enablement/Transactional Layer

Weakest Moats - Highest Vulnerability:

Possible Defensive Strategies:

- Deep Domain Integration: Embedding so deeply into industry-specific workflows that switching costs become prohibitive (e.g., specialized compliance requirements, regulatory nuances)

- Data Network Effects: Accumulating proprietary operational data that improves the solution over time in ways competitors can’t easily replicate

- Hardware-Software Integration: Building solutions that require specialized hardware or infrastructure investments

- Regulatory Compliance Expertise: Becoming the de facto standard for highly regulated industries where compliance knowledge creates barriers

Why These Moats Are Fragile: Most process optimization can be replicated by AI tools, and switching costs are typically low. The value capture is minimal, making it difficult to fund defensive R&D.

Examples: We are observing many RPA implementations being overtaken by agentic AI solutions, where even complex cognitive steps can now be automated through LLM connectivity. More advanced models go further, deploying groups of agents that collaborate to understand, define, and break down tasks into subtasks—leveraging a maker/checker paradigm to deliver more accurate and reliable outcomes.

2. Business Intelligence Layer

Moderate Moats - Medium Vulnerability:

Stronger Defensive Strategies:

- Proprietary Data Assets: Owning unique, high-quality datasets that can’t be easily acquired or replicated

- Domain-Specific AI Models: Developing industry-specific algorithms trained on proprietary data that generic AI can’t match

- Contextual Intelligence: Building deep understanding of industry nuances, regulations, and decision-making processes

- Continuous Learning Loops: Creating systems where customer usage continuously improves the intelligence, creating a widening gap over time

- Integration Depth: Becoming embedded in critical business processes where the intelligence becomes part of core decision-making

- Human-AI Hybrid Models: Combining algorithmic insights with human expertise in ways that pure AI solutions can’t replicate

Vulnerability Points: Generic AI capabilities are rapidly improving, and many insights can be commoditized. However, the combination of proprietary data + domain expertise + continuous learning can create sustainable advantages.

Examples: In our portfolio, IntelligenceNode stands out as a strong example. The company leveraged SKU-level pricing intelligence by location to accurately predict which promotions would be most effective—factoring in competitor pricing, active promotions by geography or zip code, and market dynamics. They further modeled quarterly sales and margin projections at the SKU level, rolling these up into category forecasts by region. This sophisticated use of data provided a clear competitive edge and ultimately led to their acquisition by the IPG group, which was seeking precisely these capabilities.

3. Marketplace Layer

Strong Moats - Lower Vulnerability:

Powerful Defensive Mechanisms:

- Network Effects: The more buyers and sellers, the more valuable the platform becomes—creating a self-reinforcing cycle

- Liquidity Advantages: High transaction volume makes the marketplace more attractive to both sides

- Trust and Reputation Systems: Accumulated reviews, ratings, and transaction history create switching costs

- Discovery and Matching Intelligence: Proprietary algorithms for connecting buyers and sellers that improve with scale

- Financial Infrastructure: Payment systems, escrow, insurance, and financing that create stickiness

- Brand and Trust: Becoming the “go-to” platform in an industry creates powerful incumbency advantages

- Data Insights: Transaction data provides intelligence that can be monetized or used to improve matching

- Multi-sided Lock-in: Creating dependencies where both sides need the platform to access their preferred counterparties

AI Enhancement Rather Than Threat: AI typically strengthens marketplace positions by improving fraud detection, personalization, and matching efficiency rather than displacing them.

Examples: Marketplace models inherently enjoy a strong competitive moat, as they are central to enabling discovery and managing trust—making disintermediation difficult. A good example is Mystifly, which operates a global air travel marketplace. On the supply side, Mystifly aggregates inventory from 700+ airlines—including full-service carriers, low-cost airlines, and multiple GDS/NDC integrations—through APIs. On the demand side, it connects seamlessly with OTAs, TMCs, tour operators, loyalty programs, concierge services, meta-search platforms, and even non-travel players such as fintechs, e-commerce platforms, super apps, hotels, and airports. They also streamline post-sale support by leveraging an engine that interprets and manages supply-side contract variations. Beyond aggregation, Mystifly leverages its advanced pricing engine to identify currency movements and source tickets from the most advantageous suppliers—creating arbitrage opportunities that deliver additional value to customers.

4. Product/Platform Layer

Strongest Moats - Lowest Vulnerability:

Multiple Overlapping Defenses:

- Ecosystem Lock-in: Customers become dependent on the entire integrated experience, making switching extremely costly

- Data Compound Effects: Owning the full customer journey generates comprehensive data that competitors can’t access

- Vertical Integration Benefits: Controlling multiple value chain stages creates cost advantages and better user experiences

- Customer Switching Costs: Integration depth, training, and workflow dependencies make leaving painful

- Brand and Customer Relationships: Direct ownership of customer relationships and brand equity

- Continuous Innovation Capability: Revenue scale funds ongoing R&D and feature development

- Distribution Control: Owning customer acquisition and retention channels

- Financial Model Advantages: Higher margins enable competitive pricing and investment in defensibility

Why AI Strengthens Rather Than Threatens: At this layer, AI becomes a tool for enhancing the platform’s capabilities rather than a competitive threat. The integrated nature of the offering means competitors can’t easily replicate individual AI features without rebuilding the entire ecosystem.

Examples: Credilio is India’s largest DSA-led credit distribution platform, scaling from just 3,500 agents at inception to over 40,000 active agents today. By onboarding 24+ leading banks, they significantly expanded the range of financial products available to their DSAs. Crucially, by owning both the application process and credit decision workflows, Credilio was able to spot underserved segments early—such as the opportunity to launch secured credit cards ahead of competitors. With continued access to customers’ credit data and full ownership of the distribution stack, Credilio is uniquely positioned to cross-sell additional financial products and deepen customer relationships faster than the competition.

Some Additional Insights Across Layers:

The “AI Paradox”: While lower layers face direct AI displacement risk, higher layers can use AI as a competitive weapon to strengthen their moats.

Compounding Effects: Higher layers benefit from multiple, reinforcing moats that become stronger over time, while lower layers typically rely on single-point defenses.

Capital Requirements: Building strong moats at higher layers requires more capital but generates more sustainable advantages.

Time Horizons: Lower layer moats can erode quickly, while higher layer moats often strengthen with age and scale.

The most defensible positions combine multiple moat types—for example, a marketplace with proprietary data, strong network effects, AND deep domain expertise creates overlapping barriers that are extremely difficult for competitors or AI to overcome.

~ Deepak

Learn more about: Cornerstone Ventures | CGES Index

Disclaimer:

The data provided on this website (www.csvpfund.com) is for informational purpose only.

Any information provided on this website or any of the other digital assets owned & maintained by Cornerstone Venture Partners Fund, Mumbai, India (“CSVP”)and managed by the Investment Manager, Cornerstone Ventures Investment Advisers LLP, Mumbai India, does not constitute investment advice or investment recommendation nor does it constitute an offer to buy or sell or a solicitation of an offer to buy or sell shares or units in any of the investment funds or other financial instruments.

The Cornerstone Global Enterprise SaaS Index (“CGES Index”) ™ is a trademark of CSVP. The CGES Index is created & maintained using a proprietary algorithm and is to be used for informational purpose only. It is not to be construed as an investment advice or investment recommendation in any of the constituent companies / stocks that are directly or indirectly part of the Index. The Index is created using publicly available data published on the websites of the respective companies. All data presented is as per our internal research and analysis leveraging publicly available data and is being presented only for academic deliberation and discussion purposes and is not to be viewed as any specific commentary / recommendation / evaluation / conclusion on any of the companies / stocks that are directly or indirectly part of the CGES Index.

CSVP also analyses, maintains, and publishes certain financial and non-financial metrics (“SaaS Metrics”) on the Index at an aggregate level, and not at a specific company / stock level that constitute the CGES Index. These SaaS Metrics are provided purely for informational purpose and CSVP assumes no liability for accuracy, suitability, or completeness of the SaaS Metrics. The SaaS Metrics are created using publicly available third-party information and CSVP does not claim any ownership of the sourced data. CSVP is not responsible for the accuracy, suitability or completeness of the information originally disclosed by the owner of the information and any information provided herein. CSVP accepts no liability and offer no guarantee as to whether the information is up to date, correct or complete.

CSVP may have used third-party data, information, and content (including all text, data, graphics, and logos) on the website. CSVP assumes no ownership and intends no infringement of rights, titles, and claims (including copyright, brands, patents and other intellectual property or other rights) of the respective owners or authorized users of the respective content. Use of such content is from publicly available sources and for indicative and informational purpose only in good faith. All trademarks and registered trademarks are the properties of their respective owners. This website may contain references or links to other websites. References and links to third-party websites do not mean that CSVP adopts the content behind the reference or link as its own. When first setting up the link, CSVP will have checked the linked site for illicit content and found none at that time. However, CSVP have no influence over the current and future design or content of such linked sites and will accept no liability for such content or design. Any use of these websites is at your own risk. The obligation of CSVP to remove or block the use of information according to the general laws from the time of knowledge of a concrete violation of the law remains unaffected.

X

Contact Us

contact@csvpfund.comGet our latest updates on

.svg)

.svg)

Contact Us

contact@csvpfund.comGet our latest updates on

Contact Us

contact@cornerstoneventures.vcGet the latest updates on

Cornerstone Venture Partners Fund

9 Aug 2018

IN/AIF1/18-19/0572

Cornerstone Ventures Investment Fund

11 Dec 2023

IN/AIF2/23-24/1406

Contact Us

contact@csvpfund.comGet the latest updates on

Cornerstone Venture Partners Fund

9 Aug 2018

IN/AIF1/18-19/0572

Cornerstone Ventures Investment Fund

11 Dec 2023

IN/AIF2/23-24/1406

Copyright © 2025 Cornerstone.

All Rights Reserved.